Thinking

Speaker

Books

Case Studies

Frank Schwab

I bridge the gap between Visionary

Technology and Balance Sheet Profitability

Now

available

on

Amazon

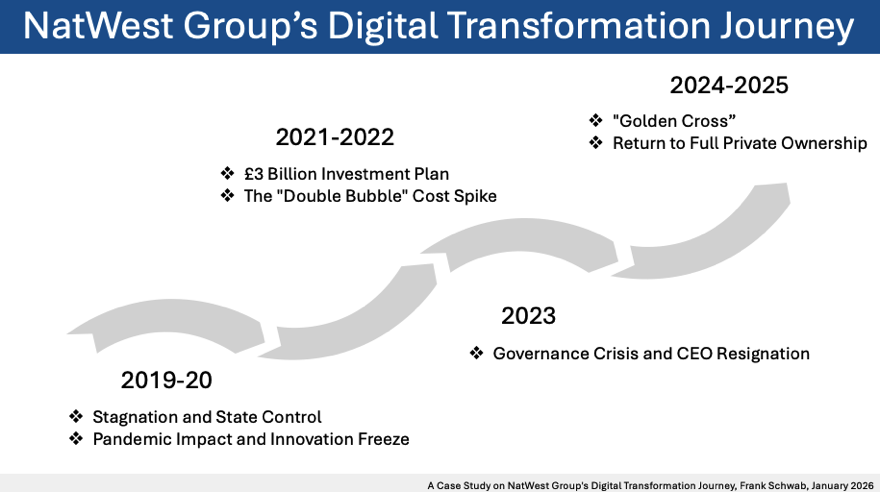

NatWest Group's Digital Transformation Journey

From Bailout to Benchmark

read all here

Beyond the Boardroom: Travel, Strategy, and Well-being

The Middle is a Death Zone:

Why Banks Must Innovate or Liquidate

30 Years Later: Building My First Python App with a Little Help from AI read all here

Decathlon & Management - Parallels Between the Decathlon and Business Leadership

🎓 Case Study: Kaspi Bank’s Digital Transformation Journey

From Almaty to the World: The Kazakh Super App

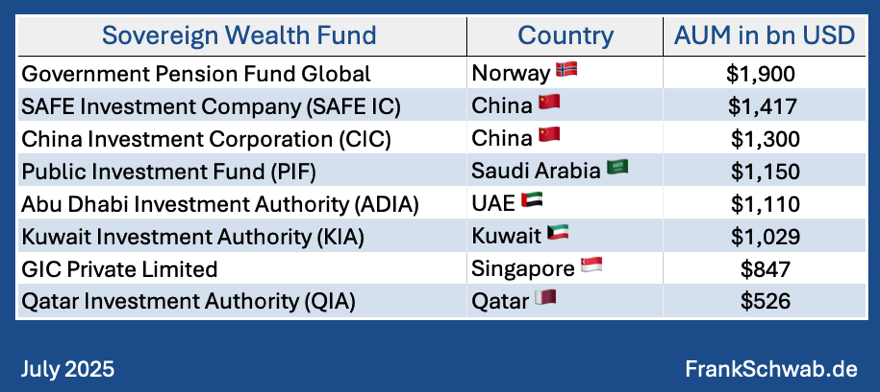

Future-Proofing Prosperity: How Sovereign Wealth Funds Turn Megatrends into Strategic Advantage

Is Your Bank Running on Borrowed Time?

Impressum

About

© Frank Schwab 2026